I can’t be the only one who reacted in a certain way after the What The Actual Fuck mini-budget? Within 24-48 hours I started to consider whether I needed to work full-time and how much money I needed to survive.

It was full-on financial apocalypse thought patterns.

My spending myths

Sometimes people inherit myths about themselves. As an example, one of the myths I’ve inherited is I don’t spend any money. The problem is this isn’t true at all, albeit sometimes I wish it was. Yet it remains. Just look at 2022 and some of the ‘bigger ticket’ items I can pick out off the top of my head: –

- A 7-day cruise to the Norwegian Fjords

- A 14-day cruise to the Canary Islands

- New PC with 3 27″ monitors

- Replaced a rather long garden fence

- Had a dense collection of six out of control conifers removed

- Scotland road trip in the van

The funny thing about this list is I’m pretty sure if I asked you to put them in order of cost you’d not get the order correct. I’m not even mentioning all sorts of periodic purchases one of which was a treadmill so they can mount up.

So what causes this myth? I can think of a few things: –

- I tend to save and then spend

- I tend to live extremely well within my means

- I put a modicum of thought into what I spend

- I forecast yearly and plan monthly

These patterns do mean I make jokes about my approach to money. I’ll joke that I think like a miser or that I live like a person much poorer than I am. The second one is particularly true but the idea that money, to some extent, doesn’t run out of my hands like water is definitely a myth.

Rising interest rates

Whether you call it luck, generational advantage, prodigious levels of planning or living well within my means I’m very fortunate and privileged because increasing interest rates are a boon for me. They are not a problem. At least not personally, existential financial failure of institutions and financial vehicles is not a topic for this blog.

I have money to save and I’ve effectively paid off the mortgage for the second time (alas the divorce wiped out the first time). I also live alone so my outgoings don’t have the money sink that is children.

Despite this, it is safe to say any processes or strategies I use to manage my money are very much a mental health mitigation because this stuff is one of the few things that can really throw me into a spiral and has done seriously in the past.

Hell, even when I spend money it can send me into an intense and momentary mental health spiral such as when the aftershock of buying the van kicked in.

Finger on the finances

The prediction is a two-year recession and that’s ignoring any financial landmines that may exist as the system struggles with ludicrously low-interest rates no longer being seen as normal. That was never normal and it established itself for way too long. The truth is until interest rates return to some level of normal and quantitative easing stops we can’t really say we’ve come out of the shadow of the 2008 financial crisis.

It’s going to be painful but hopefully not existentially shocking.

So, I’ve bolstered my finances. Nothing grand has changed it’s more an exercise in refreshing my options and tightening up the rigour and control.

- Tweaked the monthly savings funnel

- Continue to use a regular savings account

- Continue to use both types of ISA (now interest rates are better)

- Zero the mortgage account

(1) and (2) are an exercise in using savings options linked to current accounts to maximise interest rates as some of the best deals are invariably on the basis of if you have a current account with us. The regular savings account hangs off my primary current account where everything is done. The savings account and Cash ISA are with someone else who demands you have a current account but places no criteria on how it is used (win!).

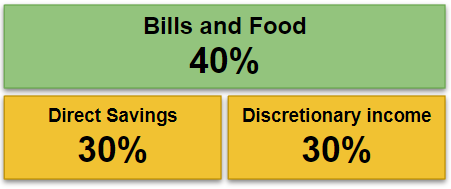

Essentially my monthly income is split into three pots: –

While the direct regular savings are a constant the other two fluctuate but they are accurate enough as an indicative monthly distribution. Yes, I realise that’s circa 60% discretionary income but I split the money into hard move savings that flow into various mechanisms directly every month and discretionary income a proportion of which will actually become savings depending on how crazy I spend. The big-ticket items listed earlier were from the 2022 discretionary income.

I have two big psychological hurdles I wrestle with in life (which I admit aren’t hardships): –

- Trying to keep discretionary income saving levels high

- Realising a I save a lot and doing something crazy might be a better option

It’s how my I could be seriously poor tomorrow brain works though and I find it hard to drag myself out of it.

What can I say about item (3)? I started a stocks and shares ISA because I needed to put money somewhere and apparently I missed the crazy assets explosion after the financial crises and post-COVID. Then the apocalyptic mini-budget triggered the doom cycle. So it’s down. At this point, I face cutting my losses or trusting the logic of just paying each month and seeing it as a ten-year investment and hoping cost averaging pays dividends. That’s the understood strategy though sometimes I wonder whether I’ve adopted this just as it becomes superfluous advice. Anyway, I’m sticking to it for now and not trying to guess the market. It’s true that less of the direct savings go into stocks and shares in 2023.

The mortgage is a technicality, there is a relatively small amount left on it that was covered by an offset savings account (it’s the method by which I’ve burned down my mortgage twice). I’ve just chosen to remove it from the savings account to the mortgage account so it displays zero. This is mostly psychological and makes what was the mortgage payment a direct to savings action rather than some weird account shuffle.

I fully recognise all these efforts are best endeavours in the face of blistering inflation but one can only do and worry about so much. After that, you have to push it out of your mind and move on. Despite all this, no one will ever persuade me I am not going to be destitute in my old age.

The van question

I am very aware of the van. This is something I remain in a big quandary about. It’s a massive asset I don’t really sweat but I have really enjoyed the 9-day trips I’ve been on. The weekend trips are not proving as great or as regular as I hoped but they are still a thing.

The trouble is once I can no longer sweat out my ancient car I’d have a monthly bill for a vehicle anyway and at least this one provides more utility. Despite this, I do occasionally think I should sell the van. This is especially true in the winter. It preys on my mind constantly.

The simple truth is there is a significant amount of capital wrapped up in the van that could be returned to me and it’s circa 20% of the money wrapped up in the regular bills and food pot.

I don’t even want to hear about other investments like property. I am realistic and have to admit this is too much for me and I would just start to regret the effort.

Reducing the work commitment

A part of me would love to do this but I’ve not done it yet. I wrestle with two dilemmas: –

- A signal to others to put my career on hold

- My role is client facing

The first one is obvious, it’s all too easy to see someone with Friday always off as a different prospect to someone working all five days. The second is manageable, but it is a factor when part of your work pattern is responding to and working with clients to some extent on their timescales. It’s not a dance to their tune thing, but neither is it a clean break.

During the pandemic, I took Friday off for 2-3 month blocks and it all worked out though, so what do I know? I also found I really liked it. A three-day weekend feels substantially longer than a two-day one.

I’m also wary of where my career may go. I work best in consultancy delivery leadership style roles. That is I am leading on how things should be done in order to turn complexity into something deliverable, then actioning some of the work myself but I also don’t mind supporting and advising others without being their actual line manager. That role is more accommodating to reducing work hours, but I sometimes wonder if due to re-organisations two things will occur.

- The client-facing element will increase

- I’ll have less of a consultancy leadership feel

- How things are done could be defined elsewhere

The challenge is depending on how the dice fall I could find I like the role substantially less but I am not particularly enamoured with seeking out pastures new at this point either. It’s something I am keeping an eye on.

The other strategy is to achieve the same thing by just buying up holidays. It’s not exactly the same though as you’d also re-arrange some of your hours if you cut out a day rather than just directly chopping off days of pay. It’s an option though.

And, Finally…

So, there you are, my post-pandemic and what the actual fuck mini-budget financial thoughts. In truth, they are relatively minor. I’m not doing anything crazy like being one of the legions of younger Boomers dropping out of the job market. I’m Gen X I have innumerable headwinds that are going to make dropping out of the job market early very challenging. A number of generational contemporaries wonder if they’ll ever be able to.

Onward and as for the next 2-3 years? Brace! Brace! And good luck.